When is flat growth considered a blessing? When it’s 2023 and flooring retailers are nearly two-thirds of the way through an obstacle course that continues to feature high inflation/interest rates, LVT slowdowns due to the UFLPA and an overall decline in retail traffic.

With Labor Day beckoning—the unofficial start of the fall selling season— flooring retailers are generally content with how the year has fared to this point, even if it lacks the robustness of recent years.

Like last year, and the years following the COVID-19 pandemic, 2023 is not what you would describe as a “normal” year—not with 7% mortgage rates, persistently high inflation and ongoing supply issues rattling retailers’ cages.

By now, however, flooring retailers know to expect the unexpected—and to adjust accordingly. “We haven’t seen anything that would be considered as a normal selling cycle since 2018; it’s really been hard to know what to expect,” said Eric Mondragon, hard surface flooring buyer for RC Willey, which operates14 locations across four western states. “Business has been on par with expectations, although we had hoped for a better Q2.”

Mondragon estimates that traffic has been down 15%-20% this year; however, RC Willey’s conversion rate is better than expected. “Customers who are coming in are definitely buyers,” he noted.

Across the landscape, flooring dealers are reporting that retail traffic is down from last year, but that average transactions are up significantly. A case in point is Barefoot Flooring in Castle Hayne, N.C. As John Bretzloff, manager, explained, “We find there are fewer customers, but we are experiencing larger tickets. Much like COVID-19, I think inflation had interrupted business for a time, but folks realize the sky is not falling and will decide to push through with their renovations or construction.”

Indeed, research shows U.S. homeowners are sitting on a mountain of equity. CoreLogic analysis through the end of 2022 showed U.S. homeowners with mortgages (roughly 63% of all properties) saw their equity increase by a total of $1 trillion since the fourth quarter of 2021, a gain of 7.3% year over year.

What’s more, Wells Fargo data revealed that U.S. homeowners have more equity in their homes today than they did at any point in the 35 years between 1987 and 2022. This home equity bonanza means there is untapped potential for consumers to rely on home equity lines of credit to sustain spending should the need arise.

But has that translated into more flooring purchases? RC Willey’s Mondragon suggested that many consumers did their home improvement projects during COVID-19 (2020-2021). “We took a lot out of the market early; now it seems that consumers are using the equity in their homes to buy recreational vehicles and to travel,” he said. “The airports and recreational areas are extremely busy. Not to mention that it is difficult to find a contractor to help with these projects. If you don’t get on their schedule early in the year, your chances of finding someone are slim.”

Inflation’s impact

What’s holding some consumers back is an unwillingness to pay the high interest rate for a second home or home improvement loan. “I do not see a great change in upward movement until interest rates begin to drop,” said Janice Clifton, owner of Napa, Calif.-based Abbey Carpets Unlimited. “In our community we have very little available in homes for sale since many homeowners are not willing to make a move to another home with the large cost of higher interest rates. Our business is mostly residential remodel, so these factors significantly affect our sales.”

Other dealers agree that, for now, higher interest rates are winning the battle over record home equity, contributing to a slowdown in store traffic. “For whatever reason, customers are just not spending like they were on home improvement projects or flooring-specific projects,” said Casey Dillabaugh, owner of Dillabaugh’s Flooring America, Boise, Idaho. “Despite high homeowner equity, interest rates for HELOC’s (home equity lines of credit) remain detrimental, so you’re not seeing that positively affect us. We do not see the retail sector correcting for the next 12-18 months—much the same as the new construction market hit us last year. Additional impacts—including but not limited to certain mills’ decisions to eliminate discount terms—will only force us to raise prices, thus negatively impacting retail flooring sales further. That said, with new construction recovering and commercial work thriving, we’re blessed to be in an incredibly healthy position as an organization.”

Despite myriad issues impacting the retail segment Kemp’s Dalton West Flooring in Newnan, Ga., is one example of a dealer that is benefiting by strong spending. “We are ahead of last year’s sales by about 3%,” said Chris Kemp, owner. “Our net profit is also up. I see more of our customers spending more money on their existing homes than they ever have before. That’s been good for our company being that we are a flooring/design type business.”

Craig Phillips, president/owner of The Flooring Edge, with three Ohio-based flooring businesses, reported business year-over-year is flat, which he considers a “blessing” given the challenges facing the flooring industry. “The reps who call on us are all reporting much weaker results out in our marketplace. I was forecasting a slight decrease at the halfway point this year after our record 2022, but I feel fortunate to be where we are. Commercial has driven our sales performance thus far in 2023 with retail being off. Stronger than expected builder business has also helped our results to date. Our retail business has shown signs of picking up after multiple months of sluggish—at best—results. Our backlog of retail business heading into August turned upward from where it sat at the end of June.

“Overall, our backlog of business is lower than it was at the beginning of the year. Some of our builders continue to see weak sales. I look for us to come up short against a strong second half last year; time will tell. A strong fall selling season may be just what the doctor ordered, though.”

Indeed, retailers who have slogged through the first two-thirds of 2023 look at the upcoming fall season as their opportunity to close out the year on a high note. “Now that summer vacations are winding down and kids start heading back to school, we’ll see if consumers get back into their normal routine of preparing for the holiday season that generally kicks off on Labor Day,” Mondragon said. “That will be the telltale sign that we are heading back to some normality and consistency in the fall/winter selling season. We also have a private sale scheduled that usually carries us through the rest of the year.”

Commercial pulse

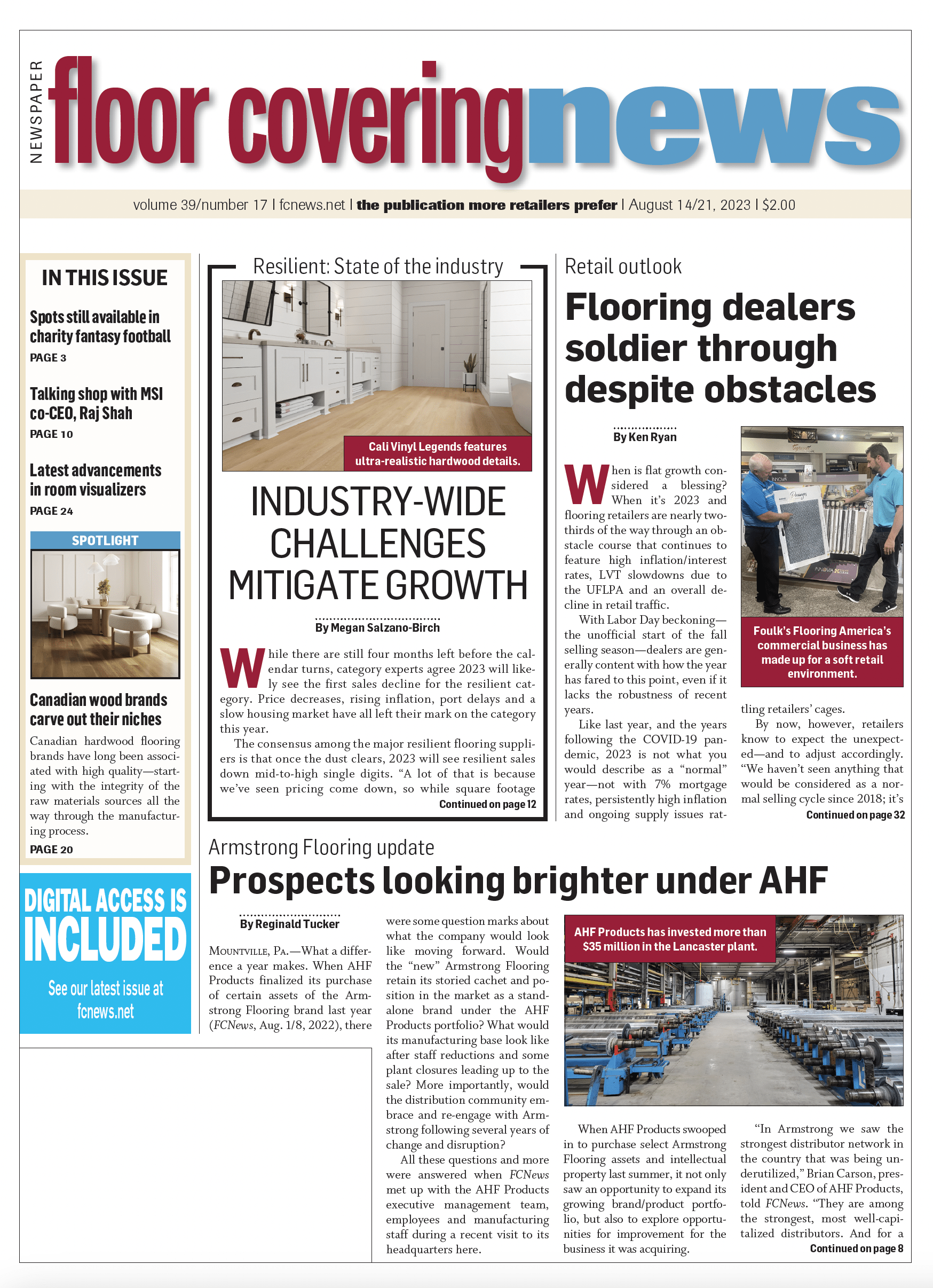

Flooring dealers with a strong presence in commercial have generally fared better than those whose business is heavily dependent on residential retail. That’s certainly been the case for Meadville, Pa.-based Foulk’s Flooring America, which reported that its business is right in line with its internal forecast. “Commercial has remained strong while retail has been soft,” said Mike Foulk, owner. “People are concerned about inflation, gas prices, etc. We expect commercial to soften some but continue to be the driving force.”

Unlike residential, the commercial sector is less impacted by interest rates. That’s good news for Abbey’s Clifton who continues to see steady sales in her commercial business. “We are down this year only about 3% from our previous year and that actually beats my expectations,” she said. “2022 was a great year for us and I’m pleasantly surprised we are only down a small amount.”

Barefoot Flooring’s Bretzloff seconded that notion, saying, “Business this year has been consistent with last year to this point, which is a bit of a surprise—and relief—given the out-of-control inflation.”