June 24/July 1, 2019: Volume 35, Issue 1

By Reginald Tucker

While several major hardwood flooring manufacturers reported modest sales increases in 2018, many will admit that profit margins were a bit tighter than they would have liked. That’s due in large part to numerous price increases enacted last year in response to rising lumber and energy costs. On top of that, portions of the category—particularly entry-level products—faced pricing pressures from the surging popularity of less expensive alternatives to hardwood, namely LVT, WPC and, more recently, SPC.

While several major hardwood flooring manufacturers reported modest sales increases in 2018, many will admit that profit margins were a bit tighter than they would have liked. That’s due in large part to numerous price increases enacted last year in response to rising lumber and energy costs. On top of that, portions of the category—particularly entry-level products—faced pricing pressures from the surging popularity of less expensive alternatives to hardwood, namely LVT, WPC and, more recently, SPC.

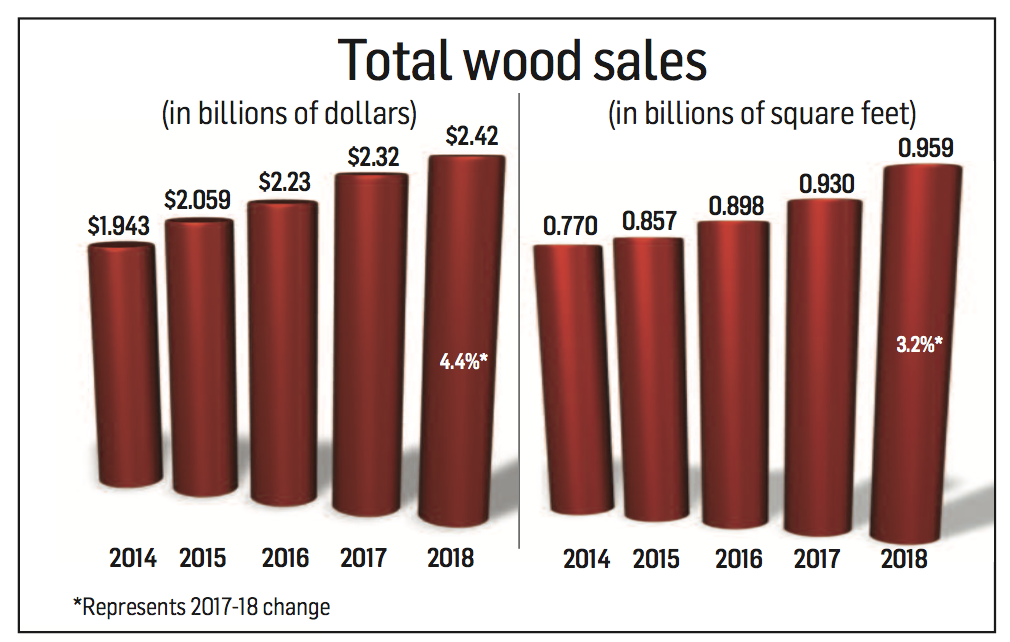

When the smoke cleared, the hardwood flooring category generated $2.422 billion in sales, a 4.4% increase over 2017. The volume of hardwood flooring sold at the first point of distribution also grew, albeit at a slower rate (3.2%), to 959 million square feet, reflecting higher-priced product and better-quality goods.

Industry observers owe hardwood’s performance to the strength of key end-use market segments. “Residential replacement continues to be the primary driver in hardwood consumption, followed by new construction—primarily single family,” said Dan Natkin, vice president of hardwood and laminates, Mannington.

Michael Bell, COO of AHF Products—the company created when Armstrong Flooring spun off its hardwood business—is in agreement. “Hardwood flooring consumption is being driven primarily by a combination of single-family new construction and residential replacement. We have enjoyed steady overall growth for the past 10 years.”

For Boa-Franc, maker of the Mirage brand, single-family construction is driving revenues followed by commercial contract and residential replacement, according to Brad Williams, vice president of sales and marketing.

Mohawk, whose gross hardwood flooring sales are up, also sees activity in the new home construction sector, especially single-family homes. Residential replacement sales are strong as well. “Commercial is strong in certain areas, but by and large it’s not a huge market for hardwood,” said Adam Ward, senior director of wood and laminate. “We don’t see those trends changing anytime soon.”

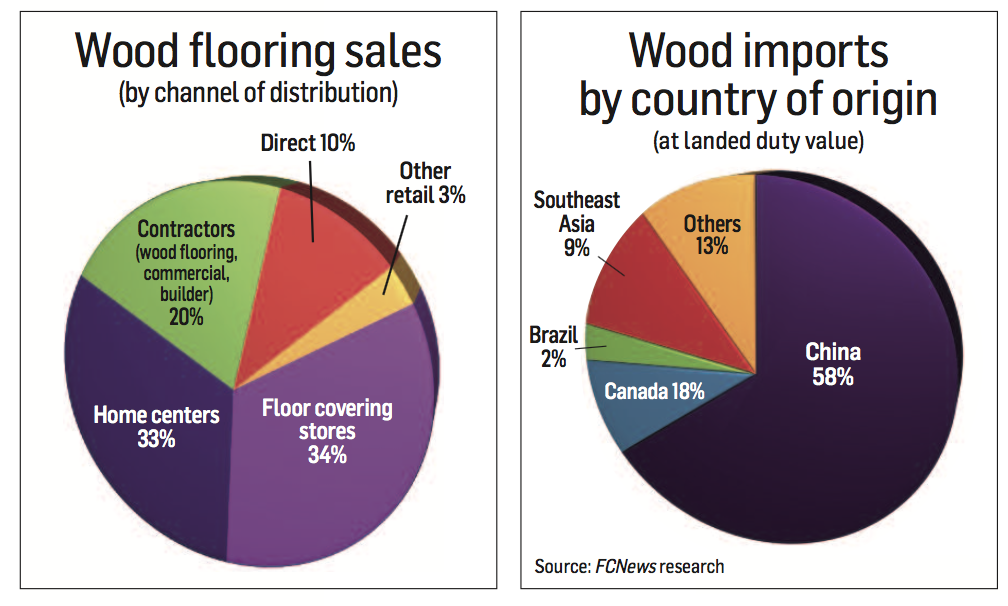

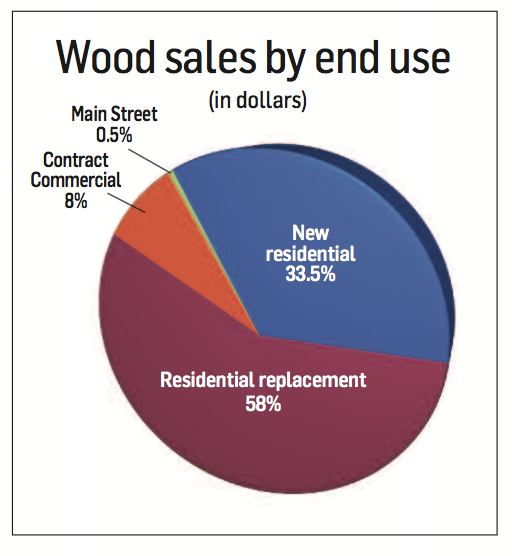

Anecdotal observations from suppliers is supplemented by hard numbers. FCNews research shows the residential replacement sector grew its share of the pie in 2018, accounting for roughly 58% of end use. That’s up a few percentage points from 2017, when residential replacement activity accounted for approximately 55% of wood sales. But that growth came at the expense of lower consumption by the new home construction sector, which fell to roughly 33.5% of sales last year compared to 35% in 2017. Commercial (specified plus Main Street) also saw its share slip in 2018, accounting for only about 8.5% of category sales. That’s off from approximately 10% of category sales in 2017.

Wood’s shifting consumption trend is more readily evident when compared to activity across other hard surface categories. In 2018, for example, hardwood represented about 17% of hard surface sales but only 10.1% of volume. Going back five years, wood accounted for nearly 20% and 15% of hard surface sales and square footage, respectively.

Much like other traditional hard surface categories, hardwood has ceded market share to the likes of trendy resilient flooring options in recent years. That’s no surprise considering many of these less expensive alternatives do an admirable job of replicating the natural visual—if not the overall heft and feel—of genuine hardwood flooring.

Bruce Zwicker, former president and CEO of Haines turned independent industry consultant, recently delivered a sobering keynote address that drove home just how much resilient flooring—both flexible and rigid core products—are nipping share from the total floor covering pie, not just hardwood. Specifically, he cited research showing LVT grew by 25% in the U.S. last year, accounting for roughly 20% of the total flooring market. By comparison, he said hardwood—although it represents approximately 13% of the total flooring space—grew by single digits.

Bruce Zwicker, former president and CEO of Haines turned independent industry consultant, recently delivered a sobering keynote address that drove home just how much resilient flooring—both flexible and rigid core products—are nipping share from the total floor covering pie, not just hardwood. Specifically, he cited research showing LVT grew by 25% in the U.S. last year, accounting for roughly 20% of the total flooring market. By comparison, he said hardwood—although it represents approximately 13% of the total flooring space—grew by single digits.

“Flooring demand in general is growing, but wood flooring demand is not,” he said. “Why is that? No. 1, the price of wood combined with the installation cost of wood makes it the most expensive floor covering. And as we all know, economic growth is not robust; disposable income is not rising at a high rate, and the standard of living in the U.S. is not growing like it used to. Hardwood is still the consumer’s aspirational choice, but flooring dealers are fighting a battle in educating the consumer that they can get more value from wood compared to some of these other products.”

Nonetheless, it’s a real issue with which wood flooring suppliers must contend. “Without a doubt, these categories are exerting tremendous pressure on the lower end of the wood category,” Natkin explained. “We have seen significant category cannibalization as vinyl-based products continue to take share. However, the mid to upper ends of the hardwood category remain strong and less prone to impact from the look-alike products.”

Observers believe the onslaught of WPC, SPC and LVT products has put many hardwood suppliers back on their heels. “It has forced hardwood to strengthen what makes it special and unique to the customers,” Mohawk’s Ward said. “However, hardwood at the upper end of the market still remains a viable option—there’s less competition there.”

Wade Bondrowski, director of sales, U.S., at Mercier Wood Flooring, attests to the toll resilient has taken on the wood market, but he’s not overly concerned. “It doesn’t seem to be affecting Mercier as much as the lower-end type products on the market” he explained. “We are finding buyers in the market for real wood typically consider better goods.”

Domestic vs. outsourcing

The gradual shift in consumer tastes is also manifested in the types of products manufacturers make domestically vs. what they import from other countries. With profit margins getting ever tighter, particularly with respect to the solid side of the business, suppliers are exploring options that make the most sense from a financial and practical point of view.

“In the U.S. today, we produce less wood flooring than we used to and we import a whole lot more,” Zwicker said. “You can actually take lumber from the U.S., ship it over to China, create a floor and ship it back to the U.S. and still be more competitive than many U.S. producers. The Chinese have lower labor costs, and the government subsidizes manufacturing there. There are anti-dumping penalties and tariffs in place to prevent unfair trade, but their costs are still really low compared to U.S. producers.”

“In the U.S. today, we produce less wood flooring than we used to and we import a whole lot more,” Zwicker said. “You can actually take lumber from the U.S., ship it over to China, create a floor and ship it back to the U.S. and still be more competitive than many U.S. producers. The Chinese have lower labor costs, and the government subsidizes manufacturing there. There are anti-dumping penalties and tariffs in place to prevent unfair trade, but their costs are still really low compared to U.S. producers.”

The import trends are reflected in the numbers. Zwicker cited research showing total flooring imports account for almost 50% of U.S. consumption, with China representing at least a third of those imports. Looking specifically at wood, however, China represents 50% of wood but 85% of LVT/multilayered flooring—the category that has been taking the greatest share from wood.

Even more telling, Zwicker said, wood imports accounted for roughly 30% of the U.S. market 10 years ago compared to 52% last year. In 2006, wood imports accounted for just 15% of the market, he said.

“The fact is producing wood flooring in the U.S. is simply not profitable for many manufacturers,” Zwicker stated. “In response, many manufacturers scaled back production, raised prices and sold all or part of their wood divisions.”

One of the companies Zwicker referenced was Shaw Floors, which earlier this year announced plans to sell its solid hardwood flooring plants to Beasley Forest Products, a vertically integrated operation based in North Carolina. The move allows Shaw to lower its production costs without disrupting the supply chain.

“We’re continually looking at how we can optimize and create value through our supply chain to make sure we’re aligned with the market,” said Herb Upton, vice president of hard surfaces at Shaw Floors.

Emerging formats

In addition to taking measures to better control costs, hardwood flooring suppliers are adapting their product offerings to better compete with the likes of WPC and SPC. In fact, many traditional wood flooring manufacturers are increasingly incorporating non-wood-based cores in their products. And now with the National Wood Flooring Association’s updated standards that classify rigid core-based floors that feature sliced or peeled wood veneers as real wood, it’s open season for this emerging format.

“These types of products have been around for years—originally on HDF cores and now evolving to vinyl or stone based,” Mannington’s Natkin said. “The latest twist is the marketing of these products as waterproof.”

“These types of products have been around for years—originally on HDF cores and now evolving to vinyl or stone based,” Mannington’s Natkin said. “The latest twist is the marketing of these products as waterproof.”

AHF Products’ Bell believes these new “hybrid” formats open the door for further innovation. “We embrace the development and evolution of core structures to ensure the hardwood customer has relevant options based on their particular needs,” he explained. “It is our job to innovate and lead in the development of such products so we are a dependable solution provider for our channel partners.”

American OEM, whose forte has long been genuine engineered hardwood, is jumping headlong into the arena with a new product called Raintree, which features a sliced veneer on top of an SPC core. “This real wood floor will be guaranteed to withstand being totally submerged in water for up to 24 hours,” said Don Finkell, CEO. “We also introduced a water-resistant, six-surface coating system on our premium products that will allow our traditional veneer core wood floors to be approved for certain wet mopping maintenance systems. We think this is a significant improvement to most wood floor warranties offered today, which disclaim any type of wet maintenance.”

Another player that has reported growing acceptance of the wood veneer/rigid core for- mat is Wellmade, which markets the Opti-Wood line of waterproof wood flooring. “Our HDPC Opti-Wood products provide dealers and distributors what they need to grow sales and improve margins in the emerging market for waterproof hardwood flooring,” said Steve Wagner, vice president of sales and marketing.

Others are taking a wait-and-see approach. “So-called hybrid products like these have the potential to be good,” Mohawk’s Ward said. “We’re obviously monitoring the products that are coming out, looking at how we can offer a superior product. While we don’t have one of those cores out yet, we want to make sure what we believe customers want in a hardwood is a real, authentic product. If we can marry that with some of the benefits—such as a water resistance or waterproof features—that makes it all the more valuable to a certain subset of customers.”

The challenge for wood flooring suppliers, observers say, is leveraging the category’s winning proposition. “All these products—LVT, WPC, SPC—are taking market share,” Zwicker said. “However, wood flooring isn’t going away anytime soon.”

Lumber pricing trends

Another factor that impacted hardwood flooring in 2018 was the escalation in raw material prices, especially for in-demand species. “Last year, we saw fluctuations in raw lumber, especially in white oak,” Mohawk’s Ward said.

Shaw Floors announced price hikes on its solid offerings last year as a result of both domestic and international demand. Upton cited the impact of an increase in shipments of logs destined for further processing in Southeast Asia as well as normal ebbs and flows of stateside demand for flooring. Also factoring into the equation, he noted, is growing demand from the other users of wood—such as mat timbers and other businesses (industrial lumber applications). “These can, over the long term, cause a major disruption in demand patterns,” he explained. “For example, we’ve seen industries such as fracking exploration impact demand for wood.”

The impact of rising demand from exports as well as domestic industries that compete for raw materials is well documented in reports provided by the Hardwood Review Weekly. The publication concluded that 2018 was by and large a good year for the U.S. hardwood industry as it ended up being the second strongest export year on record. Research shows export volumes totaled roughly 1.73 billion board feet–quite a feat considering Chinese demand tailed off significantly during the second half of the year.

The spring of 2018 in particular was particularly noteworthy with respect to export volume movement. In fact, the month of April was the highest on record for U.S. exports of red oak lumber, according to the USDA Foreign Agricultural Service data. Chinese demand for 4/4 #1C grade red oak and green #2A, 3A and kiln-dried #2A red oak remains strong as flooring plants continue to aggressively purchase lumber. FAS red oak green lumber pricing is 9% higher than a near record increase seen in July 2017. (Grades such as #1C & 2A prices were 10% and 8% higher, respectfully, during the period.)

International demand for white oak is also on the rise. Reports indicate increasing FAS grade white oak sales to Europe the, Far East and Oceanic destinations. Back at home, U.S. residential and truck-trailer flooring factories are aggressively pursuing green #2A & 3A white oak with some buying kiln-dried stock to fill gaps in supply. Sawmills also report solid orders for green #1C and better white oak from exporting concentration yards.

Overall pricing across all grades shows white oak increasing by almost 6%, with grade #1C and 2A pricing increasing 7%. The market direction for walnut, which is also rising in popularity, has shifted in recent months with demand for green exceeding kiln-dried lumber in addition to demand for grades higher than #1C and #2A. (FAS walnut lumber pricing was reported at $3,000/MBF, the highest since January 2015.) Common-grade walnut prices have followed the same trend, according to the Hardwood Review. Green walnut lumber pricing across all grades is 20% higher than the high mark seen in July 2017.

Overall pricing across all grades shows white oak increasing by almost 6%, with grade #1C and 2A pricing increasing 7%. The market direction for walnut, which is also rising in popularity, has shifted in recent months with demand for green exceeding kiln-dried lumber in addition to demand for grades higher than #1C and #2A. (FAS walnut lumber pricing was reported at $3,000/MBF, the highest since January 2015.) Common-grade walnut prices have followed the same trend, according to the Hardwood Review. Green walnut lumber pricing across all grades is 20% higher than the high mark seen in July 2017.

Pricing for cherry species is also up thanks to rising demand from China. This despite declining demand in the U.S. and elsewhere. Cherry lumber supplies are running thin, particularly green stocks, which has kept pricing up. Green lumber prices across all grades of cherry are 19% higher than those reported in July 2017. Pricing for FAS grade cherry has been on a roll since July 2014; common-grade cherry (1C and 2A) is averaging 23% higher than what was reported in July 2017.

Sawmills also report growing order files for hard maple, primarily due to demand from cabinet and wood component manufacturers. Residential flooring factories and distribution yards are buying at a steady pace at a time when hard maple is seasonally slower, according to the Hardwood Review Weekly. This combination of circumstances is compressing supplies and gradually lifting prices, particularly for the common grades, which are attracting the strongest interest. Hard maple lumber pricing in mid-2018 was 14.5% higher across all grades compared to what was reported in July 2017. (Grade 1C lumber showed the largest increase at 18%.)

But it’s not just raw materials that’s impacting the cost of wood flooring production. “We also saw transportation inflation throughout the first half of the year in 2018,” Mannington’s Natkin explained.

With respect to the impact of the tariffs on pricing, supply and demand, some executives are seeing the warning signs. “We have noticed an increase on prices to the trade, even on products not finished or sourced from regions affected by the tariffs,” said Mitch Tagle, founder and CEO of DuChateau.

Even if the imposition of tariffs on imports from China result in tangibly higher prices or reduced shipments, experts believe it won’t significantly stem the tide because it’s still more cost effective to make hardwood flooring outside the U.S. Zwicker’s research shows countries such as Vietnam, Indonesia, Cambodia and Thailand are already picking up some of the slack. “Put them all together, and they represent 17% of all the wood flooring imports coming into the country today,” he said. “That will continue to rise.”

Outlook

Despite the well-documented challenges, hardwood suppliers remain confident the category will remain viable. In fact, many are investing in their operations in anticipation of strengthening demand. Earlier this year, for example, AHF Products announced the acquisition of LM Flooring, a major producer with a global manufacturing footprint. In that same vein, Wickham Hardwood Flooring invested millions of dollars in its milling and finishing operations in Canada. Mannington also recently completed a major capital upgrade of its hardwood manufacturing plant in High Point, N.C., to enhance efficiencies and production capabilities. “There is still very strong fundamental demand for hardwood,” Natkin told FCNews.

Another factor leaning in wood’s favor is the outlook for residential remodeling spending—a critical end-use sector for the category. A newly released report from the Joint Center for Housing Studies of Harvard University showed homeowners spent $339 billion on remodeling in the first quarter of 2019, a 7% increase from a year earlier. More importantly, consumers are expected to lay out $345 billion in the second quarter, up 6.9% year on year, according to the center.

By the first quarter of 2020, spending on home remodeling is projected to reach $347 billion, an increase of 2.6%. This compares with estimated expenditures of $352 billion in the third quarter of 2018, a 6.9% rise from a year earlier, and $353 billion in the fourth quarter of 2018, a 5.2% uptick over 2017.

“Home improvement and repair spending has been in an extended period of above-trend growth for several years, due to weak homebuilding, aging homes and other factors,” said Abbe Will, associate project director at the center’s Remodeling Futures Program.

On the downside, suppliers expect raw materials pricing fluctuations to continue to be a challenge, remaining higher than this time last year. “We expect to see increases across all species, with red oak being the most volatile,” AHF Product’s Bell said. “We have also experienced significant inflation in freight and packaging.”

All in all, though, suppliers expect to see movement in the right direction. “As we look further into 2019, we expect to see slight to modest growth,” Shaw Floors’ Upton said. “We’re predicting growth around 5% for the hardwood category.”

Mirage’s Williams predicts a slower increase than what the industry experienced in 2018. “We project the overall hardwood category will see a modest growth rate of 3% for 2019.”