June 24/July 1, 2019: Volume 35, Issue 1

By Reginald Tucker

After a robust 2017, the U.S. housing market in 2018 showed it is only human. According to statistics compiled by the U.S. Census Bureau, single-family starts rose 3.2% to 876 million units—a slower rate than what we saw over the 2016–17 period, when single-family starts grew nearly 8.6%. On the plus side, total starts (including single- and multi-family) inched up 3.9% in 2018 to 1.25 million units. That’s up compared to the 2016–17 period, when total starts grew nearly 2.5%.

After a robust 2017, the U.S. housing market in 2018 showed it is only human. According to statistics compiled by the U.S. Census Bureau, single-family starts rose 3.2% to 876 million units—a slower rate than what we saw over the 2016–17 period, when single-family starts grew nearly 8.6%. On the plus side, total starts (including single- and multi-family) inched up 3.9% in 2018 to 1.25 million units. That’s up compared to the 2016–17 period, when total starts grew nearly 2.5%.

From a regional standpoint, the greatest activity was seen in the South (630 million units) followed by the West (336 million units). The Midwest and Northeast regions accounted for 173 million and 111 million units, respectively.

One of the biggest surprises was the performance of the multi-family sector, where starts increased 5.6% in 2018 to 374 million units. That marks a dramatic about-face from the 2016–17 period, when multi-family starts actually decreased almost 9.7%.

Like housing starts, single-family building permits also rose in 2018. U.S. Census Bureau figures reflect a 2.3% uptick to 1.31 million permits last year. However, that growth rate is down significantly from the 2016–17 period, when permits grew 6.2%. On the flip side, multi-family permits dipped just over a percentage point last year from 462 million to 457 million.

Robert Dietz, chief economist at the National Association of Home Builders (NAHB), cited the dynamics behind the changing U.S. housing market. “For the past several years, shortages of labor and lots—along with rising regulatory costs—have led to a slow recovery in single-family construction. While home price growth accommodated increasing construction costs during this period, rising mortgage interest rates coupled with the cumulative run-up in pricing has caused housing demand to stall.”

According to a Wall Street Journal article, single-family home building stagnated in 2018 after steadily climbing throughout the economic expansion that began roughly eight years ago. Construction of multi-family buildings in particular continued to ease as the market for new condominiums and apartments cooled, the article added.

Despite strong economic growth and a historically low unemployment rate, factors that would typically support homebuyer demand (i.e., a shortage of inventory and rising borrowing costs) have locked out many potential buyers. And while house price inflation has slowed, it continues to outpace wage growth, sidelining some first-time home buyers. “The residential construction market hit the pause button in 2018,” said Aaron Terrazas, senior economist at Zillow, an online real estate database.

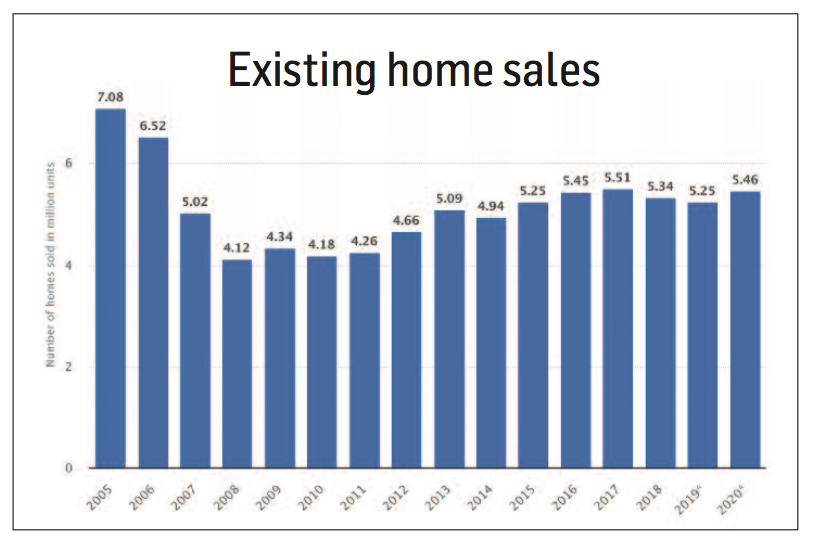

Another indication of the pulse of the market in 2018 was the rate of existing home sales. According to the National Association of Realtors (NAR), 5.34 million existing homes were sold last year—down 3% from 2017. Meanwhile, 667,000 newly constructed homes were sold in 2018, up roughly 3% from the year prior. Meanwhile, investment in homebuilding contracted 0.3% in 2018, the biggest drop since 2010.

Mid-year reportThe year 2019 kicked off on a high note as seasonally adjusted housing starts reached 1.29 million units in January, a whopping 13% increase over the last month of the previous year. However, that rally was short-lived as starts fell roughly 11% in February 2019 to 1.149 million seasonally adjusted units before inching up 1.6% to 1.168 million seasonally adjusted units in March. Then, inexplicably, starts kicked up again in April, growing 5.7% to 1.235 million seasonally adjusted units. More importantly, both single- and multi-family segments saw consecutive monthly gains from February through March.

In May, however, the brief momentum stalled. Privately owned housing starts reached a seasonally adjusted annual rate of 1.269 million units, 0.9% below the revised April estimate of 1.281 million and 4.7% below the May 2018 rate of 1.332 million units. Single-family housing starts in May totaled 820,000, 6.4% below the revised April figure of 876,000.

Meanwhile, building permits in May—the most recent period for which reliable statistics are available—hit a seasonally adjusted annual rate of 1.294 million, which is 0.3% above the revised April rate but 0.5% below the May 2018 rate of 1.301. By comparison, privately owned housing completions in May were at a seasonally adjusted annual rate of 1.213 million units, 9.5% below the revised April estimate of 1.34 million units and 2.8% off the May 2018 rate of 1.248 million.

Current sentiment among major builders is telling. A newly released report showed falling confidence among builders surveyed by NAHB and Wells Fargo, whose jointly produced HMI Index fell two points to 64 in June. (The NAHB Housing Market Index is a gauge of builder sentiment on the relative level of current and future single-family home sales. A reading above 50 indicates a favorable outlook on home sales; below 50 indicates a negative industry outlook.) Sentiment levels have held at a solid range in the low- to mid-60s for the past five months.

“While demand for single-family homes remains sound, builders continue to report rising development and construction costs, with some additional concerns over trade issues,” said Greg Ugalde, NAHB chairman.

Continued housing market weakness could be signaling a slowdown in the overall economy, observers say. Residential investment contracted in the first three quarters of 2018, the longest stretch since mid-2009, reports show. The decline in homebuilding investment that became evident in the fourth quarter of 2018 is expected to persist through the first half of 2019 as the sector continues to adjust to higher mortgage rates. (The 30-year fixed mortgage rate has increased more than 60 basis points this year to about 4.63%, according to mortgage Freddie Mac.)

Continued housing market weakness could be signaling a slowdown in the overall economy, observers say. Residential investment contracted in the first three quarters of 2018, the longest stretch since mid-2009, reports show. The decline in homebuilding investment that became evident in the fourth quarter of 2018 is expected to persist through the first half of 2019 as the sector continues to adjust to higher mortgage rates. (The 30-year fixed mortgage rate has increased more than 60 basis points this year to about 4.63%, according to mortgage Freddie Mac.)

“Home prices remain some- what high relative to incomes, which is particularly challenging for entry-level buyers,” NAHB’s Dietz said. “And while new home sales picked up in March and April, builders continue to grapple with excessive regulations, a shortage of lots and lack of skilled labor that are hurting affordability and depressing supply.”

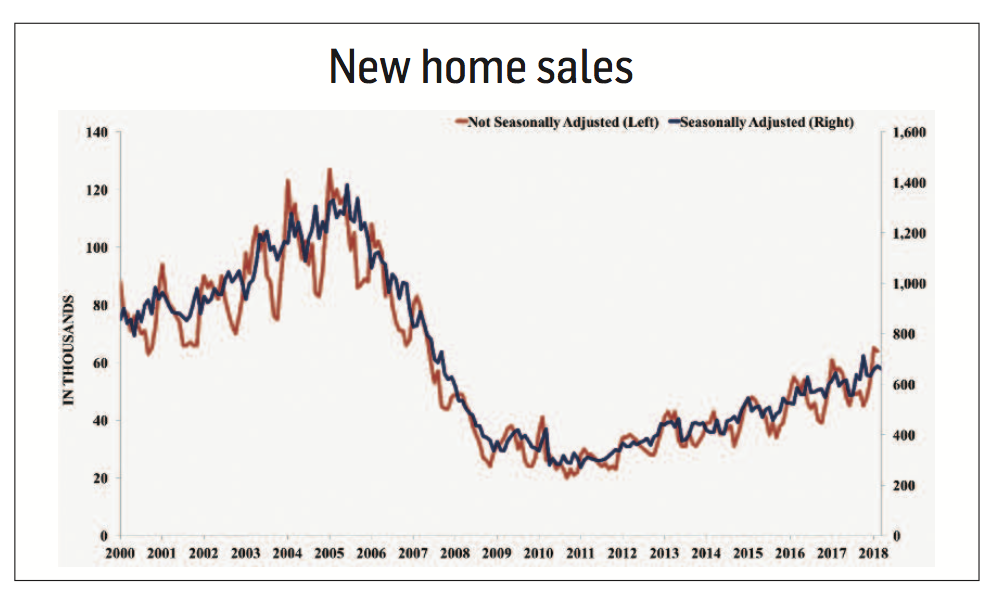

New home salesAccording to estimates supplied by the U.S. Census Bureau and the Department of Housing and Urban Development, sales of new single-family homes in April 2019—the most recent period for which reliable estimates are available—hit a seasonally adjusted annual rate of 673,000. That’s 6.9% below the revised March rate of 723,000 but 7% above the April 2018 estimate of 629,000. The median sales price of new houses sold in April 2019 was $342,200, with the average sales price hitting the $393,700 mark.

New home sales in the South, which accounts for the bulk of transactions, increased 3.6% in March to their highest level since July 2007. Sales in the Midwest soared 17.6%, while those in the West surged 6.7%. However, sales in the Northeast tumbled 22.2%. About 62% of the houses sold in April were either under construction or yet to be built. Analysts say new home sales have not been severely impacted by the supply problems that have plagued the market for previously owned homes.

With respect to inventories, the seasonally adjusted estimate of new houses for sale at the end of April was 332,000. This represents a supply of nearly six months at the current sales rate.

Despite the broader housing market’s struggles with supply, industry observers believe the fundamentals for housing are generally improving. The 30-year fixed mortgage rate has dropped by about 80 basis points since November, according to Freddie Mac. That followed a recent decision by the Federal Reserve to suspend its three-year monetary policy tightening campaign.

In addition, home price inflation has slowed and wage growth has picked up. At the same time, land and labor shortages are constraining builders’ ability to break more ground on lower-priced housing projects.