June 26-July 2, 2018: Volume 34, Issue 1

By Reginald Tucker

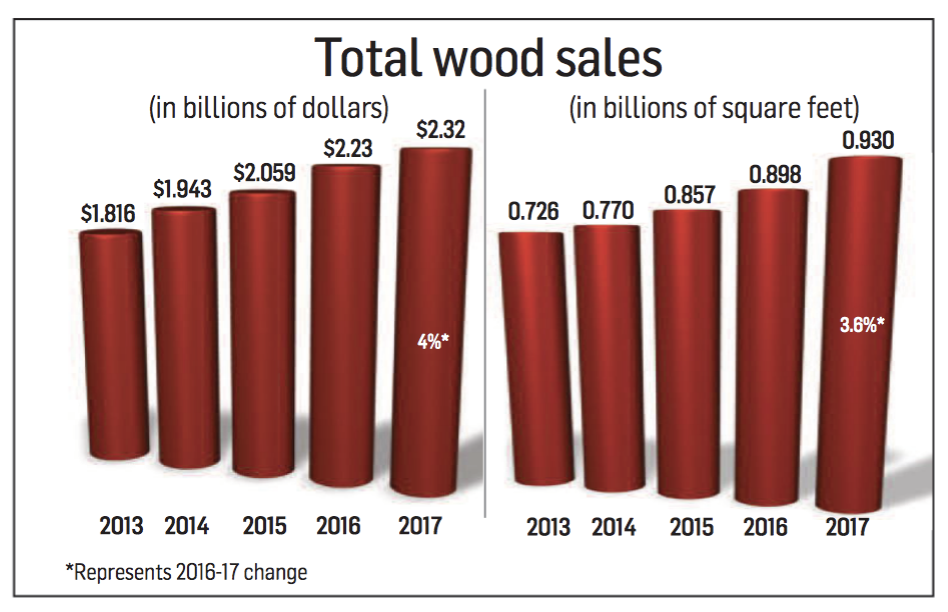

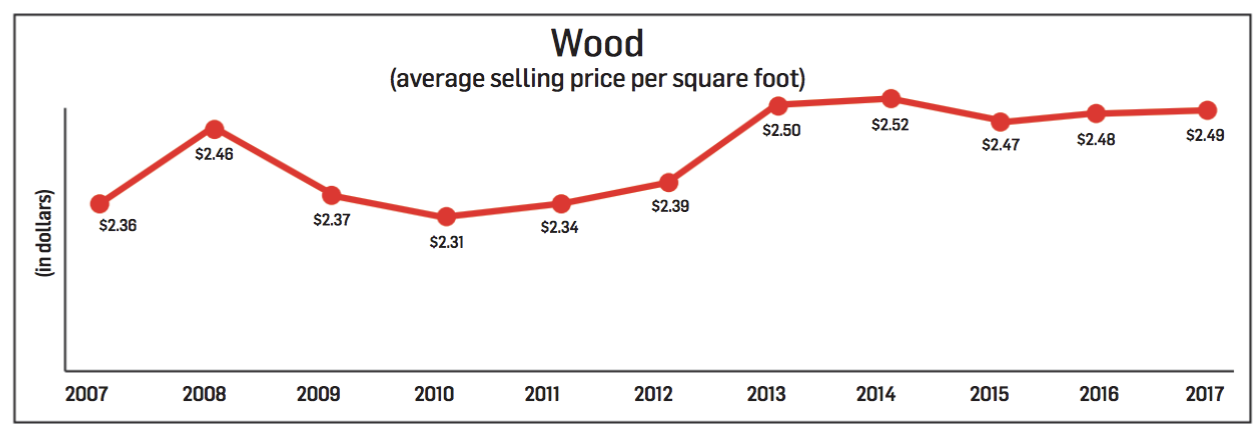

Rising demand for residential replacement projects combined with a strengthening new home construction market contributed to another steady year of growth for the U.S. hardwood flooring industry. FCNews research shows wood sales at the first point of distribution climbed to $2.32 billion in 2017, a 4% increase over 2016. Volume-wise, units shipped increased 3.6% to 930 million square feet, reflecting an uptick in slightly higher-value goods.

Rising demand for residential replacement projects combined with a strengthening new home construction market contributed to another steady year of growth for the U.S. hardwood flooring industry. FCNews research shows wood sales at the first point of distribution climbed to $2.32 billion in 2017, a 4% increase over 2016. Volume-wise, units shipped increased 3.6% to 930 million square feet, reflecting an uptick in slightly higher-value goods.

To put the numbers in greater perspective, in 2017 the hardwood sector accounted for nearly 10.6% of total industry sales but more than 17% of hard surface revenues. With respect to volume, wood represented only 4.7% of total industry square footage shipped but 11% of all hard surfaces sold at the first point of distribution. Five years ago, wood’s share of total industry sales was 9.5%, while its share of total industry volume was 4.1%. Going back even further—to 2007—hardwood’s share of total industry sales was 9%, while its share of volume sold was 4.4%. However, the size of the total pie at that time was much greater—$22.34 billion in sales in 2007 vs. $17.3 billion in 2012. Ditto with respect to volume; in 2007, more than 22.7 billion square feet of product was shipped compared to just over 16.8 billion in 2012.

While evidence shows competing hard surface categories seem to be growing at a faster clip (save for laminates), wood has not ceded its position relative to its ranking among the likes of tile, resilient flooring, WPC, etc. For example, wood represented the third-largest hard surface category in terms of dollars in 2017, trailing only resilient (19.2% market share of total industry sales) and tile (13.3% of total sales). Back in 2007, wood was also the third-largest hard surface category—although resilient and tile represented a much lower portion of the overall pie at 9.8% and 9.3%, respectively. Ten years ago, wood held a 9% share of the market. The only oddity is the volume of wood sold has been exceeded by the overall square footage of laminate flooring shipped virtually every year since 2009. Industry observers attribute this phenomenon to a variety of factors, including: much lower comparative pricing of laminate vs. wood; the relative ease of installing laminate flooring vs. more complex, intricate hardwood flooring products; and the vast number of retail outlets—including big boxes and discount stores—that sell laminate over the counter and online.

Industry executives attribute hardwood’s consistent performance over time to the strength of key end-use sectors here in the U.S. market. “Single-family construction and residential replacement continue to be the core drivers of demand for  hardwood,” said Dan Natkin, vice president, wood and laminates, Mannington. “While the wood category grew by low single digits, the growth rates were different between solid and engineered, with solids declining in overall volume and engineered growing by mid-single digits.”

hardwood,” said Dan Natkin, vice president, wood and laminates, Mannington. “While the wood category grew by low single digits, the growth rates were different between solid and engineered, with solids declining in overall volume and engineered growing by mid-single digits.”

Other executives, including Natalie Cady, vice president, hard surface marketing, Shaw Floors, concur. “Residential is driving the market, which includes both single family and residential remodel.”

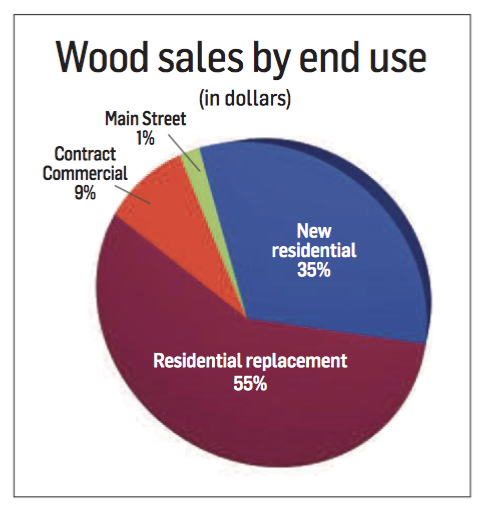

FCNews research supports those anecdotes. In 2017, residential replacement and new construction end-use markets accounted for 55% and 35%, respectively (or 90% collectively), of hardwood flooring sales. That’s up slightly from 2012, when new residential and residential replacement represented about 83% of category sales. One of the biggest shifts over that time period occurred in the commercial sector, which—including specified contract and Main Street market applications—accounted for 17% of sales. Last year, contract commercial and Main Street represented just 10% of sales, research shows.

The fact that hardwood is still be able to participate across a variety of end-use channels is a testament to the segment’s allure and viability. “A more stable economic environment continues to steer the hardwood segment on a course of steady growth, with increases in demand in both the new construction and remodeling markets,” said Michael Bell, vice president, hardwood, Armstrong Flooring. “We also see hardwood opportunities in the commercial marketplace.”

Other industry observers, including Brad Williams, vice president of sales and marketing at Boa-Franc, parent company of the Mirage brand, believe commercial performed better than many expected. In fact, as far as the ratio of end-use consumption is concerned, he feels a shift has occurred. “I believe single-family construction is driving the most growth in hardwood, followed by contract commercial and residential replacement.”

Shifting formats, trends

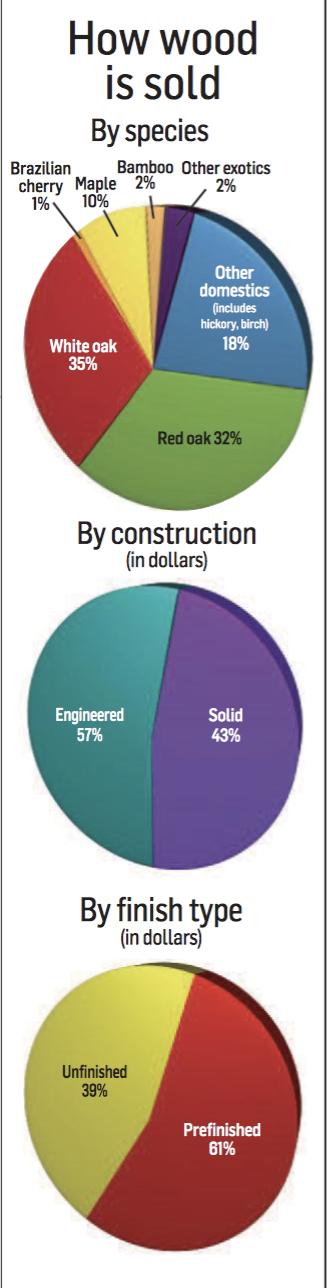

While several industry executives continue to debate the precise ratio of end-use consumption, there’s no denying there is an industry-wide shift in the types of hardwood floors produced and sold. Take traditional solid hardwood floors— the mainstay  in many regional markets—vs. the preponderance of new, technologically advanced engineered formats. Ten years ago, solid wood floors represented more than 60% of the market, anecdotal information shows. According to FCNews research, the engineered/prefinished segment is close to overtaking solids, accounting for roughly 57% of sales.

in many regional markets—vs. the preponderance of new, technologically advanced engineered formats. Ten years ago, solid wood floors represented more than 60% of the market, anecdotal information shows. According to FCNews research, the engineered/prefinished segment is close to overtaking solids, accounting for roughly 57% of sales.

While solid—what some refer to as the industry “gold standard”—is still preferred by many customers, home builders and designers in markets like the Northeast and Pacific Northwest, the rapid development and evolution of products that fall under the category of engineered floors is opening up opportunities even in hardcore solid markets.

“There’s never been more changes taking place in the wood flooring segment than what we’re seeing today,” said Tom Lape, president, Mohawk Residential. “The biggest trend we’re seeing in the wood flooring segment today is a blurring of the lines within the product categories. For example, we’re clearly seeing many customers, dealers and consumers moving away from solid at a rate that has been running unabated for five years running and continues to accelerate. We see the engineered category evolving right in front of our eyes from what was historically a 5-ply construction format to an HDF product solution.”

Mohawk is so convinced that engineered wood flooring products based on an HDF core are quickly overtaking conventional, multi-ply hardwood flooring options that it is banking on wholesale consumer and end-user acceptance of the emerging format. “When you see high-end custom builders and high-end production builders in the Northeast and Pacific Northwest coming off solid it is eye opening,” Lape said. “Solids are not going away, but where there is a reasonable trade off of in terms of cost, value, etc., I think you’re seeing the market accelerate the move to engineered.”

Boa-Franc’s Williams is in general agreement. “The shift in demand will continue to put additional pressure on manufacturers as the majority of domestic suppliers have solid equipment and capacity. This causes your business to transform when converting to producing engineered, or more engineered vs. solid. Everything changes—from your lumber purchasing to your go-to market channel strategy.”

For others, the continued migration from solid to engineered doesn’t necessarily spell the end of a category. While engineered floors offer opportunity for design innovation combined with its installation flexibility, solids still have their place. As Armstrong’s Bell explained: “The dynamics are different in solid vs. engineered. In engineered, we see much of the growth occurring on the bookends of the market with significant increases in the opening price point/value engineered products and the best/premium sliced- and sawn- face engineered products. Solid is similarly seeing increased activity on the best/premium side of the market.”

While it is generally accepted that consumer tastes differ by region and/or climate, some point to inherent limitations of solid products as an impediment to acceptance beyond the core solid markets. “With the demand and overall trend moving toward longer and wider, there are limitations you have solids that are not there with engineered,” Shaw Floors’ Cady said, citing the tendency of solid floors to expand and contract more easily than engineered. “Having the ability to go longer and wider will help people move more toward engineered. Plus, with single-family home construction on the rise, that represents an increase in concrete slab construction— and that lends itself to engineered. At the end of the day, we believe the solid market— which includes both finished and unfinished product—is steady, not actually shrinking.”

While it is generally accepted that consumer tastes differ by region and/or climate, some point to inherent limitations of solid products as an impediment to acceptance beyond the core solid markets. “With the demand and overall trend moving toward longer and wider, there are limitations you have solids that are not there with engineered,” Shaw Floors’ Cady said, citing the tendency of solid floors to expand and contract more easily than engineered. “Having the ability to go longer and wider will help people move more toward engineered. Plus, with single-family home construction on the rise, that represents an increase in concrete slab construction— and that lends itself to engineered. At the end of the day, we believe the solid market— which includes both finished and unfinished product—is steady, not actually shrinking.”

In keeping with the industry’s ongoing transition to engineered, suppliers are also seeing demand move away from traditional strip flooring to wider/longer plank formats. “We’re giving consumers more of what they want,” Mohawk’s Lape stated. “We’re selling planks up to 80 inches long x 9 inches wide, and we’re making better-performing products for contractors, retailers as well as consumers.”

While all this continues to play out, suppliers continue to fortify—and diversify—their product mix to ensure they have all the bases covered. Over the past 18 months, for example, Quebec-based Wickham Hardwood introduced several new engineered offerings designed to complement its solid collections. According to Paul Rezuke, vice president residential sales, U.S., the breakdown seems to follow along geographic lines. “As part of our engineered strategy, we targeted two platforms based on a 1⁄2- and a 3⁄4-inch format. We initially envisioned the 1⁄2-inch product would be most suited for the U.S. market and the 3⁄4-inch line for our Canadian business partners. What we are seeing is the demand in the U.S. market for a thicker platform appears to be on the rise. With this demand, we are projecting a significant demand for 3⁄4-inch platform engineered products in our U.S. footprint.”

The shift in product preference in wood goes beyond the product’s core construction. Industry observers are also gauging changing consumer tastes relative to color, species, surface texture and even board length and width. “The key is making sure we stay out in front in terms of styling and design,” Shaw Floors’ Cady explained. “We’re still seeing the move toward longer, wider planks, but we are also seeing a move toward more traditional visuals.”

At the other end of the spectrum, some suppliers are seeing a mild resurgence in demand not for domestic species—which had been rising in popularity—but for exotic looks. With anecdotal information and consumer purchasing trends showing shoppers gravitating more toward home- grown species such as walnut, hickory and birch, to name a few, others say there’s still a viable market for imported tropical species.

“Brazilian cherry, teak and oak are still in demand,” said Luxia Hong, director of business development, North America, for Grupo Maderero Amaz, based in Peru. “What we’re doing is taking the Brazilian teak, for example, and applying wirebrushing to the top layer. We can also apply stains such as gray, espresso and cappuccino—the colors that are trendy today. Brazilian oak can also take stains and wire brushing very well.”

Mitigating factors

Hardwood flooring has long been linked to its ability to con- tribute to rising home values, and it remains—as suppliers argue—the product that many homeowners covet. But aggressive competition from competing “wood-look” visuals available with LVT, WPC, laminate and, now, ceramic is a cause for concern.

“The growth of wood-look products such as WPC is an issue,” Mannington’s Natkin said. “While cannibalization is minimal for the consumer who really desires hardwood, there is conversion for consumers who are not sure what product is right for them.”

Armstrong’s Bell is in agreement, adding that—with the exception of tile—most of these products cost less than real hardwood. Also at play, he said, is the fact that the quality of the visuals and textures has evolved so much that many consumers feel comfortable using these faux wood products instead of the real thing. “However, there is nothing that can truly compete with genuine hardwood from either a look or value equation. It is a great, long-term investment and can actually become a strong resale argument, exceeding the initial installation cost of the floors. Plus, it’s organic, natural and renewable and, of

course, since it is natural, has less pattern repeat.”

Traditional, hardwood-only suppliers seem to be taking it in stride. As Wickham’s Rezuke explained, “Currently, WPC appears to be the category of the month. We’ve experienced this in the past with both laminate and LVT. Our position remains that there will be new products that will present challenges. But in thelong run, hardwood will always maintain a significant market share in the flooring industry.”

Price pressures

On the other side of the coin, wood’s classification as a natural product also subjects the category to price fluctuations due to rising raw material costs. In fact, some of the segment’s top suppliers recently announced hikes in the 3%-7% range, mostly on solid goods. Suppliers warn it might not be the last this year.

“We are seeing some upward pressure in raw material pricing,” Mannington’s Natkin said. “Certain regions are more dramatic than others.”

“We are seeing some upward pressure in raw material pricing,” Mannington’s Natkin said. “Certain regions are more dramatic than others.”

Armstrong, one of the suppliers to pass on increases to its customers earlier this month, attributes the hikes to rising natural gas and electricity prices—all of which impact costs to power the plants. Bell doesn’t see any let up in sight. “We expect this cost pressure to continue throughout 2018.”

Canada-based Mercier Wood Flooring, which instituted a price increase at the start of the year, hinted at the possibility of additional hikes if cur- rent trends persist. “We try to stay consistent,” said Wade Bondrowski, director of sales, U.S. “However, a couple more increases in raw materials and we will be forced to raise prices again.”

Boa-Franc, also based in Canada but services customers throughout North America, is feeling the pinch as well. “We are still sitting at a high point on species such as red oak and white oak,” Williams said. “Hopefully it will cool down and stabilize in the quarters to come.”

Mid-term outlook

Despite raw materials fluctuations, pricing pressure from imported product and increased competition from other hard surface categories, executives remain optimistic about the hardwood sector for the remainder of 2018. “We predict the overall hardwood category will have a moderate growth rate of 3%-5% this year,” Williams said, citing the commitment of its distribution partners. “We feel our greatest opportunity continues to be within our existing network.”

Don Finkell, president and CEO, American OEM, is confident the category as a whole

will grow by at least 6% this year, surpassing the rate of growth achieved in 2017. The prospects look even better from an internal standpoint, he noted. “I expect our company to more than double that growth rate at about 12% to 15%. We are adding new products for our existing distributors, building on our private-label programs and developing coverage of our new Hearthwood brand. Plus, we will be adding more domestically made products to our Hemisphere brand.”

Others are similarly bullish. “We’re still forecasting growth in the wood segment, although I think it’s going to be a different wood segment by virtue of a lot of trends we’ve been talking about,” Lape stated. “The trend is going to be more innovation in the wood category. The industry is not sitting still; it continues to innovate in terms of form, function and value.”

For Mercier, the key to continued success lies in geographic expansion—along with continued development of its engineered program. “In a number of areas, the Mercier line is fairly new,” Bondrowski said. “But with the amount of design and quality we have and continue to pursue, these markets could use a product line like ours.”

For Shaw, opportunities abound both within industry wide. “The launch of our premium brand, Anderson Tuftex, will bring about some exciting new possibilities,” said Drew Hash, vice president hard surface product category management. A strengthening housing market can’t hurt, either. “The greatest opportunities for hard- wood products are within single-family and new construction. We continue to expect an increase in housing starts, which will have an impact on growth throughout 2018.”

Rising demand sends lumber pricing higher

By Reginald Tucker

Rising demand for hardwood flooring products resulted in a steady rise in lumber prices across a range of species in 2017, a trend that is expected to continue at least throughout 2018. That’s according to data released by Forecon, a forestry consulting firm with in-depth knowledge of the U.S. lumber industry. Forecon reports high demand for red oak, hard maple, ash and cherry (the latter due to mostly export demand). Red oak, which has set record export levels in volume and dollars this past year, is also seeing robust demand domestically.

Those findings are corroborated by statistics cited in the latest Indiana Forest Products Price Report and Trend Analysis published in January. According to the report, pricing for premium species such as red oak and white oak—often viewed as the primary market/economic indicators in the hardwood industry—is trending higher. White oak lumber (#2/Btr) prices are 3% higher than what was reported in July 2017, while red oak prices are almost 6% higher. Aside from domestic demand—especially among sectors like millworking and cabinetry suppliers, which compete for raw materials—industry observers cite strong

export activity to China. Current pricing for red oak, especially #2/3A red oak, is at levels not seen since January 2015. The most popular kiln-dried grade red oak, #1C, is increasingly high in demand among Chinese and Vietnamese suppliers.

Pricing for green upper-grade red oak lumber (FAS & FIF) peaked at $1,370 per thousand board feet (MBF) in the summer of 2014. Prices for FAS lumber spiraled downward through early 2016 before rising to the current price of $1,150 MBF. Both #1C and 2A pricing have been increasing since January 2016 to $845 and $560 MBF, respectfully.

White oak pricing is also seeing a bump, with most of the upper-grade lumber heading to the Far East and Europe. Here in the States, white oak demand by hardwood flooring producers is rising. Upper-grade white oak pricing has increased steadily since January 2016 to its current

price of $1,650 MBF. This price is also 38% higher than what was reported in July of 2013. Further, #1C and #2A pricing has also firmed quite well with increases of 34% and 7%, respectively.

Other species commanding high prices include: upper-grade green walnut ($2,900 MBF). According to the report, #1C prices are over 47% higher than in July 2013 and 16% higher than the figured reported in July 2017. Meanwhile, the cherry market continues to rebound, primarily due to Chinese demand. Upper-grade cherry prices are trending 16% higher than the year-ago period, with common grades averaging 13% higher than those reported in July 2016.

Lastly, upper-grade hickory lumber prices are nearing levels reported during the summer of 2015—a high point for the product. The overall average of hickory lumber prices are 7% higher than the fall of 2016.