June 26-July 2, 2018: Volume 34, Issue 1

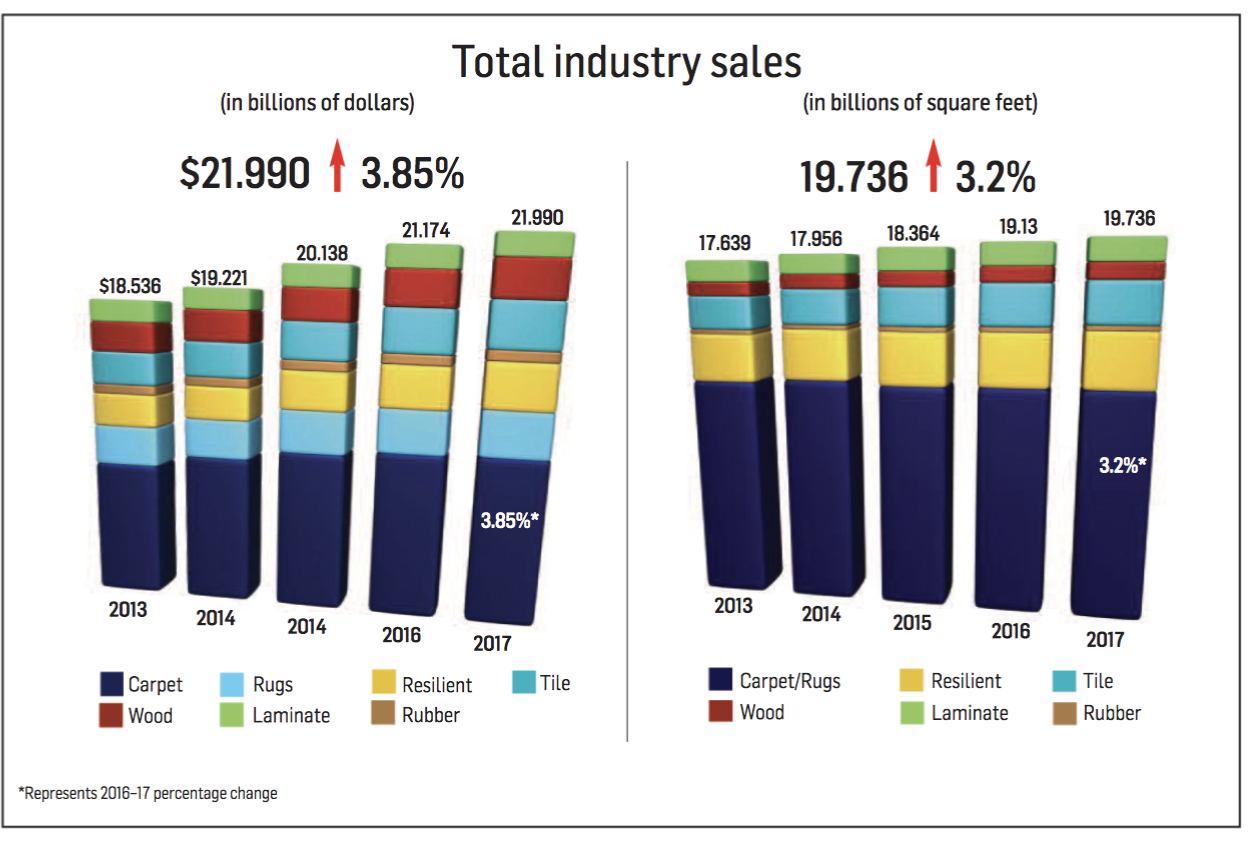

The flooring industry in 2017 continued its prolonged climb back from the economic slump that plagued the United States from 2007-2010, led by the resilient category in general and everything waterproof in particular. While growth rates pale in comparison to the mid-2000 heydays, the industry last year continued to post steady gains across the board with increases of 3.85% in dollars and 3.2% in volume. This comes on the heels of 5.1% growth in dollars and 3.8% in volume in 2016; 4.4% growth in dollars and 3.2% in volume in 2015; 3.6% growth in dollars and 1.8% in volume in 2014 and respective 5.5% and 3.8% growth in 2013. In fact, 2017’s figures represent the eighth consecutive year of dollar growth and sixth straight year of volume increases.

The flooring industry in 2017 continued its prolonged climb back from the economic slump that plagued the United States from 2007-2010, led by the resilient category in general and everything waterproof in particular. While growth rates pale in comparison to the mid-2000 heydays, the industry last year continued to post steady gains across the board with increases of 3.85% in dollars and 3.2% in volume. This comes on the heels of 5.1% growth in dollars and 3.8% in volume in 2016; 4.4% growth in dollars and 3.2% in volume in 2015; 3.6% growth in dollars and 1.8% in volume in 2014 and respective 5.5% and 3.8% growth in 2013. In fact, 2017’s figures represent the eighth consecutive year of dollar growth and sixth straight year of volume increases.

FCNews’ exclusive research reveals total 2017 flooring sales topped out at $21.990 billion and 19.736 billion square feet. (These numbers are in wholesale dollars reflecting the first point of sale. They also do not include stone flooring, nor does it account for ceramic wall tile, cove base and rubber accessories.) While the industry remains far off the peak it reached in 2006, when sales of $24.175 billion and 26.36 billion square feet (down 9% and 25%, respectively) were posted, it has gained back much of what was lost. The low point for the industry was 2009, when sales bottomed out at $16.189 billion and 16.625 billion square feet (in 2010). Since that time, the industry is up nearly 35.8% in dollars and 18.7% in volume. The greater growth in dollars is a reflection of consumers buying more expensive goods along with a series of price hikes, particularly on the carpet and hardwood sides. Perhaps even more significant is total industry sales approaching $22 billion, a plateau that has not been reached since 2007, when sales were $22.337 billion. Volume is also fast approaching 2008’s 19.905 billion square feet. But keep in mind that 10 years ago, FCNews included cove base and accessories in its rubber flooring numbers. Last year we made the decision to include only sheet and tile flooring in our rubber numbers and only adjusted back to 2012. In the absence of that change, 2017’s numbers could have eclipsed 2007’s sales and 2008’s volume figures.

The average selling price of all flooring in 2017 was $1.11 (the same as 2016 and 2015, and up $0.02 from 2014 and $0.04 from 2013). Just to compare, the average selling price of all flooring in 2006 was $0.94.

One needs only to look at the resilient category for an explanation. Eleven years ago, the average selling price for all resilient flooring was $0.64. These past two years it has been $1.04. A decade ago, sheet vinyl, vinyl composition tile (VCT) and the low-cost, peel-and-stick tile commanded 75% of dollars. Last year that number plummeted to 28.8%, down from 33% in 2016. The increased usage of the higher-cost LVT, both residentially and commercially, and now WPC have been industry game changers. But it’s not just resilient. The average ceramic tile price has increased from $0.95 to $1.19 a square foot over the last 10 years, and hardwood has seen an average-square-price jump from $2.21 to $2.49 per square foot. Even the maligned soft surface segment—which has seen its share of the market dip from 64% in 2007 to 51.8% in 2017 (and down from 53.7% in  2016)—has seen an increase in average pricing from $0.89 to $1.01. For the record, laminate is the only category with pricing in decline, going from $1.32 a square foot in 2007 to $1.09 in 2016. It dipped a half-cent in 2017 to $1.085. Laminate is also the only category in 2017 to show a decline in both dollars and volume, primarily due to lower domestic production capacity in 2017 and the growing popularity of WPC, ceramic tile and lower-priced wood and bamboo flooring. Why has the growth been slow and steady and not more robust? For one, housing has not led the recovery from the recession and is actually lagging the economy. While it continues to rebound and grow each year, housing starts are still below the 1.4 million threshold that is considered normal. Also, in past recoveries, there has always been a period of strong economic growth before it settles into normal growth mode. That has not happened with this recovery.

2016)—has seen an increase in average pricing from $0.89 to $1.01. For the record, laminate is the only category with pricing in decline, going from $1.32 a square foot in 2007 to $1.09 in 2016. It dipped a half-cent in 2017 to $1.085. Laminate is also the only category in 2017 to show a decline in both dollars and volume, primarily due to lower domestic production capacity in 2017 and the growing popularity of WPC, ceramic tile and lower-priced wood and bamboo flooring. Why has the growth been slow and steady and not more robust? For one, housing has not led the recovery from the recession and is actually lagging the economy. While it continues to rebound and grow each year, housing starts are still below the 1.4 million threshold that is considered normal. Also, in past recoveries, there has always been a period of strong economic growth before it settles into normal growth mode. That has not happened with this recovery.

But there have been many positives. The U.S. economy continues to grow as consumer spending (due to rising employment) and household income (and with it, disposable personal income) are on the rise. Commercial construction continues to rebound, and corporate pre-tax profits grew in 2017 after a sub-par 2016.

Also, not to be underestimated as a flooring market driver, is an aging baby boomer population. Boomers control the lion’s share of this country’s disposable income and are in their prime spending years. Many are buying second homes, or at the very least transitioning into different places of residence.

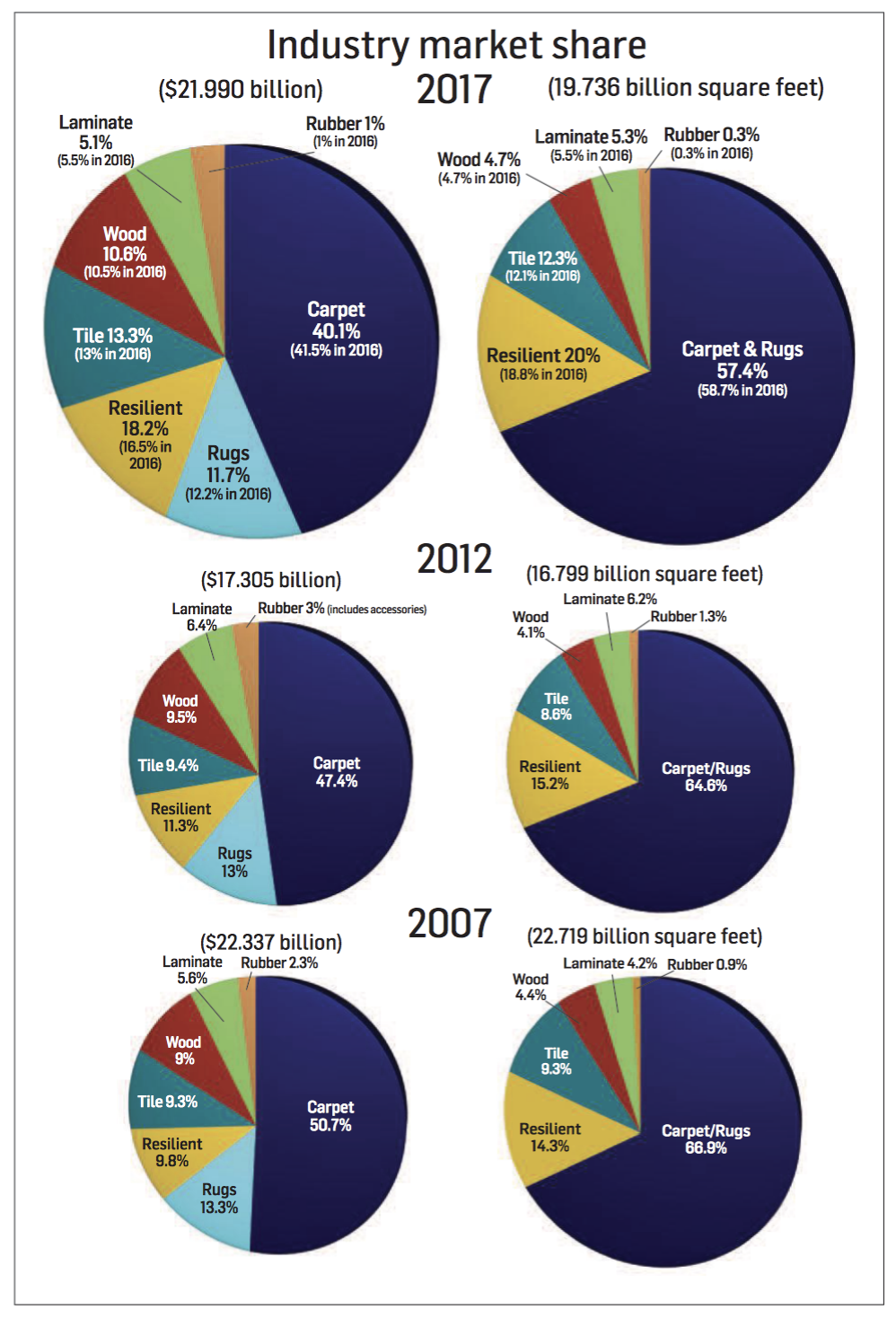

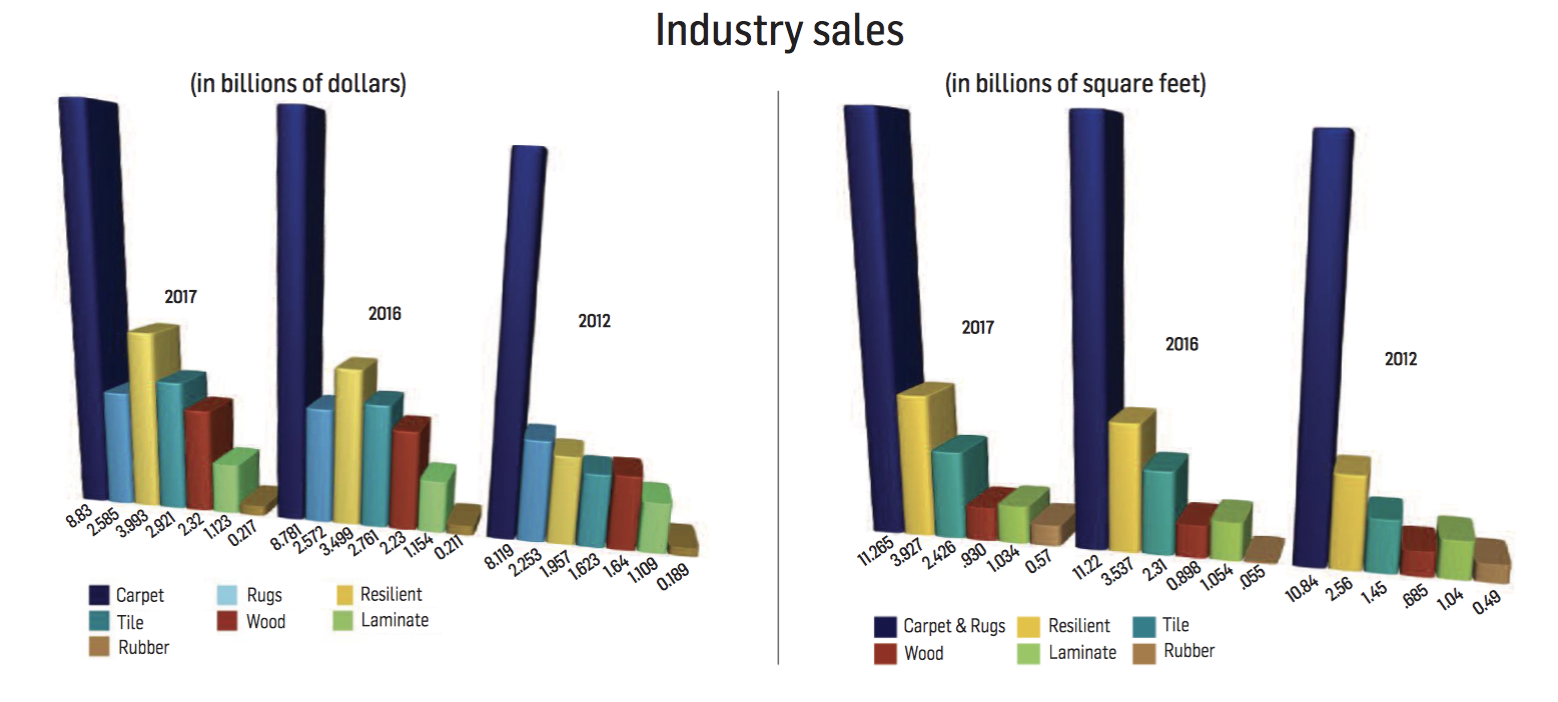

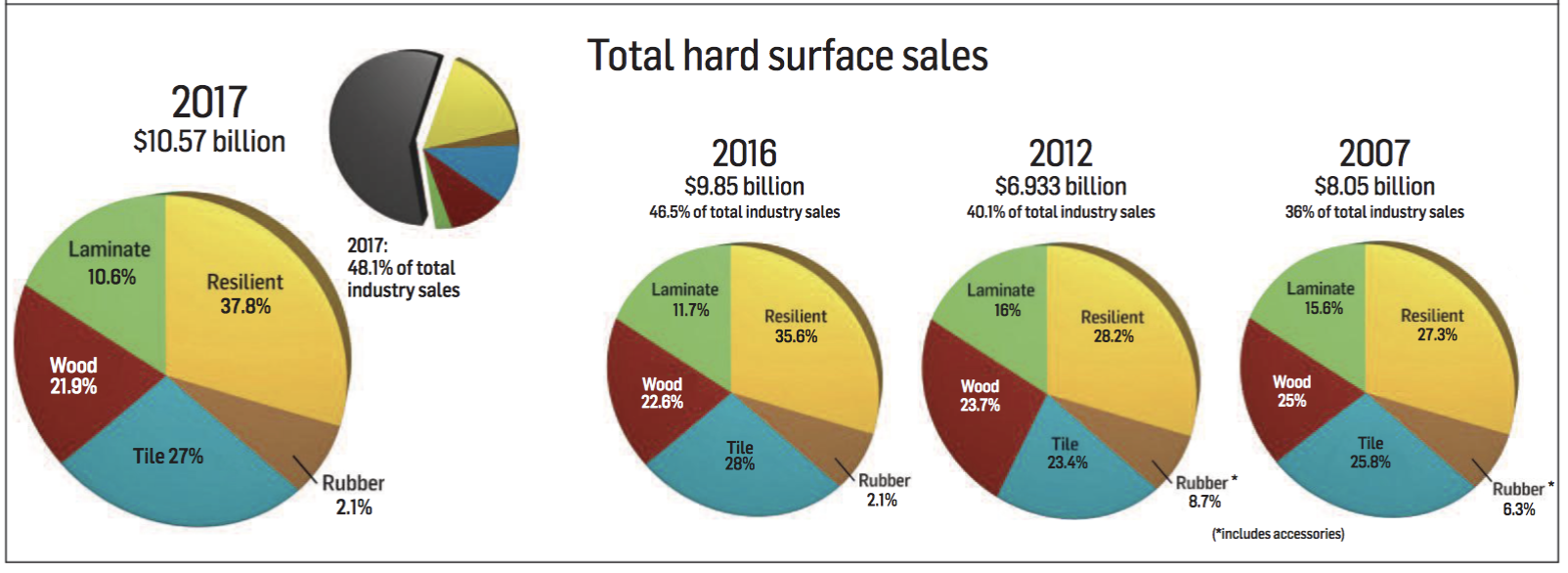

Much like the past few years, the resilient category continues to be the locomotive powering the industry and WPC the catalyst for this explosive growth. In 2017, resilient posted the largest percentage gain of any flooring category, rising 14.1% to $3.993 billion from $3.499 billion in 2015. Since 2010, the category has increased a stunning 132% and is now is at its highest point in history in terms of dollars. Interestingly, it has “only” increased 68.1% in volume, again accentuating the migration from felt to fiber-glass sheet, along with the transition from residential/ commercial sheet and VCT to LVT and WPC.

In the grand scheme of things, resilient now accounts for 18.2% of the total flooring market in dollars (up from 16.5% in 2016) and 20.4% in volume (up from 18.8% in 2016) after a 13.8% rise in units to 4.024 billion square feet. In 2015, resilient held a 13.3% market share in terms of dollars, which was up from 12.2% in 2014, 11.9% in 2013 and 11.2% in 2012. Interestingly, its market share in volume had stayed around 15% for eight consecutive years until leaping to 17% in 2015 and 18.8% in 2016.

FCNews research reveals just how much LVT—along with its sub-category, WPC/rigid core—is driving growth of the segment. LVT sales have gone from nearly $750 million in 2012 to $2.685 billion in 2017. That means the category has grown two-and-a-half timesin five years. But it is no longer sufficient to strictly talk about LVT. WPC/rigid core has taken on a life of its own with 2017 sales of $936.3 million (92.4% residential) and 480.25 million square feet (93.1% residential). To put this in perspective, WPC/rigid core now comprises 34.9% of all LVT and 45.8% of all residential LVT sales in dollars. In terms of volume, WPC/rigid core constitutes 25.9% of all LVT and 31.8% of all residential LVT. And at $1.95 per square foot, it is the most expensive resilient flooring product aside from linoleum and rubber.

LVT in general also carries with it a premium price tag as it comprises 63.8% of the category’s dollars but only 45.5% of its volume. To illustrate its growth, those numbers were 37.4% and 20.6%, respectively, in 2012.

LVT increased significantly in both residential and commercial markets—dollars and square feet—in 2017. Residential LVT saw a 32.6% increase in square footage from 1.04 billion in 2016 to 1.379 billion (including WPC/rigid core), making up 74.2% of the LVT market. This number was 76% a year ago and 71% two years ago. The big increase can be attributed to the WPC bandwagon, which, to this point, is almost exclusively residential. The commercial market rose from 297.2 million square feet in 2015 to 326.3 million square feet (9.8%) in 2016 to 478.6 million square feet, a 46.7% increase. This can be attributed to many commercial carpet mills (Bentley, Milliken, Interface and others) getting into the LVT game through third- party sourcing from companies like Nox and Gerflor, not to mention organic growth from the likes of Shaw/Patcraft, Mohawk, Mannington and Armstrong. While residential brought in significantly more dollars—$1.888 billion—last year, commercial LVT still performed well, posting a 22.9% increase, rising from $648.6 million in 2016 to $796.5 million in 2017.

Proponents of the category say the versatility of LVT—tile or plank—makes it an ideal solution for any number of residential, commercial and project-oriented applications. This multitasking ability has allowed LVT to migrate into builder, multi-family and residential-remodeling applications. The large space in which LVT operates, in turn, has afforded manufacturers the means of introducing differentiated product across a wider front, ebbing the march toward commoditization.

Originally, LVT became popular as a water-resistant, hard sur- face product ideal for mainly kitchens and sometimes spaces such as a laundry room. In the past, LVT would not be considered for bedrooms or other larger living spaces throughout the home. However, this perception has changed in recent years.

As LVT grows, it is taking share from other resilient categories, especially VCT, which today is only 7.5% of resilient dollars and 13.6% of volume. Five years ago, those numbers were 19.7% and 26.8%, respectively. But it is also nipping from sheet vinyl as well. Sheet vinyl—residential and commercial combined—has grown only 1.5% in the last four years, going from $791 million in 2013 to $803 million in 2017. It actually was down 0.8% from $809.6 million in 2016. Residential has led the way here, but if not for the rebound in new home construction and manufactured housing, sheet vinyl would surely have shown a more precipitous drop. The commercial market has taken the bigger hit, declining 11.9% in dollars from $254.24 million in 2013 to $224 million in 2017. The category has been a challenge for just about everyone, with heterogeneous continuing to take share from homogeneous, which really has only three players remaining: Armstrong, Mannington and Tarkett. On a more positive note, commercial sheet was flat in 2017 on the heels of 1.2% and 1.4% declines in the two prior years. It remains a mainstay in healthcare, where a more seamless floor covering is demanded.

Sheet has been the perennial volume leader in residential resilient sales, but it is losing its stronghold with the growth of LVT, particularly the WPC/rigid core sub-segment. Last year, sheet vinyl maintained a 42.3% share of the residential market, down from 47% in 2016, 55.1% in 2015 and 60.2% in 2014, but it comprises only 22.4% of dollars, down from 26.7% in 2016 and 38.9% in 2015. And if one is to group LVT and WPC together, residential sheet loses its volume leadership by nearly six percentage points. Sheet is also a favorite of homebuilders, which favor its ease of installation, attractive styling and good  value.

value.

Carpet

It was a year of change for the category in 2017 as two longstanding mills vacated the market, including former No. 3 player Beaulieu, which was acquired by Engineered Floors out of bankruptcy. Last year also saw multiple rounds of price increases as companies contended with increases in raw material costs. In the end, carpet sales rose a scant 0.6% to $8.83 billion while volume inched up 0.4% to 11.265 billion units.

For the second year in a row, residential outperformed commercial. In fact, carpet volume was down 6% by some estimates in the commercial sector, while sales fell about 3%. Residential carpet sales, meanwhile, increased 2.5% while units were a tad lower. The sales increase was helped by the trend toward better goods in the marketplace as well as several rounds of increases that took place over the course of the year.

Overall, carpet and rugs make up 57% of the flooring market in terms of volume, still the largest percentage of any flooring surface, yet down from its dominant days of a decade ago when it commanded 66.9% of the industry.

Carpet is still expected to lose share to hard surfaces in 2018 and perhaps future years, but there is sentiment that the slide will at least slow down. Industry observers cite two rea- sons: today’s technology is producing luxuriously soft carpet that is also durable and stain resistant, and consumers have shown the inclination to invest in the better goods, even if it is just for their bedrooms. Second, and perhaps more importantly, an aging population prefers softer, warmer surfaces such as carpet vs. laminate and other harder surfaces, according to studies.

Carpet tile, although strictly a commercial product, now represents 60% of the soft market in commercial and continues to grow across most sectors. Rugs is another soft product that has enjoyed a resurgence, albeit with the help of hard surface’s growth. While rugs increased an estimated 3.4% in 2017, most of that growth is not occurring in the specialty retail channel. After three years of relative flatness, carpet sales—at least residentially—are expected to climb a few percentage points in 2018, a reflection of the strong economy and improving housing market.

Ceramic

“Let the good times roll” could be the theme for the ceramic tile category, which has posted eight consecutive years of growth, including jumps of 5.8% in sales and 5% in volume in 2017—the second-largest segment gain next to resilient. That growth translated into ceramic tile sales of $2.921 billion last year, the third-highest amount of all floor coverings and the second-largest sales volume with respect to hard surfaces. The ratio was much the same with respect to volume, as the amount of ceramic tile sold at the first point of distribution hit 2.426 billion square feet—second only to resilient.

As much as any category in flooring, ceramic has a symbiotic relationship with housing. When housing metrics are positive, the ceramic business usually follows suit. Looking at the overall U.S. economy in 2017, gains in the construction and housing markets, as well as historically low interest rates and falling unemployment, lifted ceramic tile to its third straight year of 5% growth or better.

Much like carpet and resilient, ceramic tile consumption is closely tied to housing activity. One industry consultant told FCNews housing starts fell by 70% during the recession, and during that period ceramic tile sales plummeted by more than 30%. Now that housing starts are progressing at a moderate pace, ceramic tile is participating in the resurgence.

While the ceramic tile market has grown eight consecutive years and bears little resemblance to the 2007-2009 period, when sales and volume each fell 20% or more in consecutive years, its growth has been constrained to some extent by a continuing shortage of labor and, to a lesser extent, the massive growth of LVT and its sub-segments. Still, most executives believe ceramic will continue to grow in the mid-single digits— and possibly higher—in the years ahead.

Wood

The hardwood flooring category—the fourth-largest sector behind tile—also posted respectable numbers last year, largely due to strong residential replacement activity as well as continued consumption by the new home construction sector. FCNews research shows wood sales at the first point of distribution climbed to $2.32 billion in 2017, a 4% increase over 2016, while volume shipped increased 3.6% to 930 million square feet. Like resilient and ceramic, the closing gap in the ratio of percentage growth of sales to volume reflects greater movement of more expensive materials (i.e., advanced multi-ply engineered floors as well as higher costs due to price increases).

With hardwood’s performance in 2017, the sector now accounts for nearly 10.6% of total industry sales. When compared to total hard surface sales, wood’s share expands to more than 17%. On the volume side, however, it represented only 4.7% of total industry square footage shipped, but 11% of all hard surfaces sold in 2017.

With hardwood’s performance in 2017, the sector now accounts for nearly 10.6% of total industry sales. When compared to total hard surface sales, wood’s share expands to more than 17%. On the volume side, however, it represented only 4.7% of total industry square footage shipped, but 11% of all hard surfaces sold in 2017.

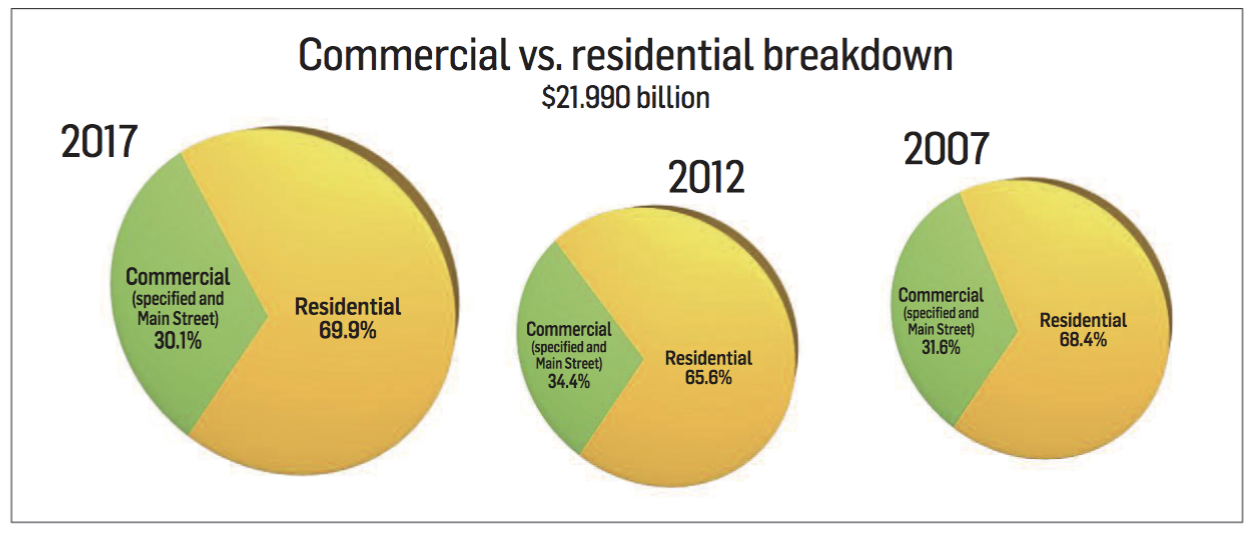

A closer look at the end-use channels helps explain the growth trend. In 2017, residential replacement and new construction end-use markets accounted for 55% and 35%, respectively (or 90% collectively), of hardwood flooring sales. That’s up slightly from 2012, when new residential and residential replacement represented about 83% of category sales. One of the biggest shifts over that time period occurred in the commercial sector, which— including specified contract and Main Street market applications—accounted for 17% of sales. Last year, contract commercial and Main Street represented just 10% of sales, research shows.

While industry research along with anecdotal evidence shows competing hard surface categories seem to be growing at a faster pace, wood has not ceded its position relative to its ranking among the likes of tile, resilient flooring, WPC, etc. For example, wood represented the third-largest hard surface category in terms of dollars in 2017, trailing only resilient (18% market share of total industry sales) and tile (13.3% of total sales). Back in 2007, wood was also the third-largest hard surface category—although resilient and tile represented a much lower portion of the overall pie at 9.8% and 9.3%, respectively. Ten years ago, wood held a 9% share of the market.

Laminate

The one category that did not experience year-over-year growth in both sales and volume in 2017 was laminate. FCNews research shows sales of laminate in the U.S. fell 2.7% to $1.1.23 billion with volume shipped at the first point of distribution to 1.034 billion square feet, down 1.9% compared to 2016. Industry observers cite, among other factors, a shift in imports and the loss of significant domestic capacity when one major supplier closed its U.S. laminate operations.

The 2017 falloff in laminate flooring sales put the category totals at their lowest level since 2013, when sales reached just over $1.12 billion before rising each year for three consecutive years. Likewise, the volume of laminate flooring sold hit its lowest point since 2011, when shipments totaled 1.02 billion square feet. The contrast is even more pronounced when comparing last year’s activity to laminate’s performance 10 years ago; at that time, U.S. sales hit $1.169 billion, with volume reaching roughly 970 million square feet. While laminate still exceeds hardwood in the volume department (albeit slightly), the category is among the lowest in terms of price per square foot. In fact, the segment has not seen much movement beyond the $1.08 per square foot wholesale price point since 2010. Meanwhile, competing products such as resilient and ceramic tile have seen their respective price points increase accordingly.

The 2017 falloff in laminate flooring sales put the category totals at their lowest level since 2013, when sales reached just over $1.12 billion before rising each year for three consecutive years. Likewise, the volume of laminate flooring sold hit its lowest point since 2011, when shipments totaled 1.02 billion square feet. The contrast is even more pronounced when comparing last year’s activity to laminate’s performance 10 years ago; at that time, U.S. sales hit $1.169 billion, with volume reaching roughly 970 million square feet. While laminate still exceeds hardwood in the volume department (albeit slightly), the category is among the lowest in terms of price per square foot. In fact, the segment has not seen much movement beyond the $1.08 per square foot wholesale price point since 2010. Meanwhile, competing products such as resilient and ceramic tile have seen their respective price points increase accordingly.

Observers are also seeing big boxes and discount merchandisers grow their market share. FCNews research shows Home Depot and Lowe’s increased their share of laminate sales to the tune of a combined 46%, up from 42% in 2017. That’s in keeping the big-box giants’ market share of laminate sales in 2012.